The market for hot water

Health and wellness is spiking — sauna and cold plunge especially in a post-COVID world — and bathhouses are wildly underserved in America. The comps below show what established thermal-bath operators pull in, and how long they last. Click any column header to sort.

Global wellness economy growing 7.6%/yr; wellness tourism 9.1%/yr. Sources: Global Wellness Institute, 2025 Global Wellness Economy Monitor (2024 data) & Thermal/Mineral Springs research (2024). Prior draft used 2020–22 figures ($5.6T, $436B) — updated to current GWI data.

The undersupply

Bathing establishments cluster in Asia and Europe; the entire rest of the world — including the US — is a sliver of the 31,386 global total. The category is also accelerating: ~365 new springs/bathing venues opened 2020–25, with 250+ more in the pipeline.

| Region | Thermal bathing establishments ▼ |

|---|

Asia and Europe establishment counts: GWI (2022 data). "Rest of world" is the residual against the 2024 global total of 31,386 — the US alone is a small fraction of it (an older GWI estimate put it near 337). Regions use slightly different vintages; treat as directional.

Thermal bath comps

What established operators do on visitors, price, revenue, and footprint.

| Operator | Annual visitors | Admission price | Admission revenue | Size (sf) |

|---|

Admission price as posted range; revenue and size rounded as reported. Submersive (Austin) is the closest comp — a 15k sf immersive bathhouse projecting $117 avg ticket / $14M revenue; its investor pitch is the template this concept adapts. Ten Thousand Waves (Santa Fe) tiers $64 communal / $89 private and has run 40+ years. Figures from operator sites and pitch materials — directional, not audited.

Thermal bath longevity

These places last. Staying power, in years open.

| Establishment | Years open ▼ |

|---|

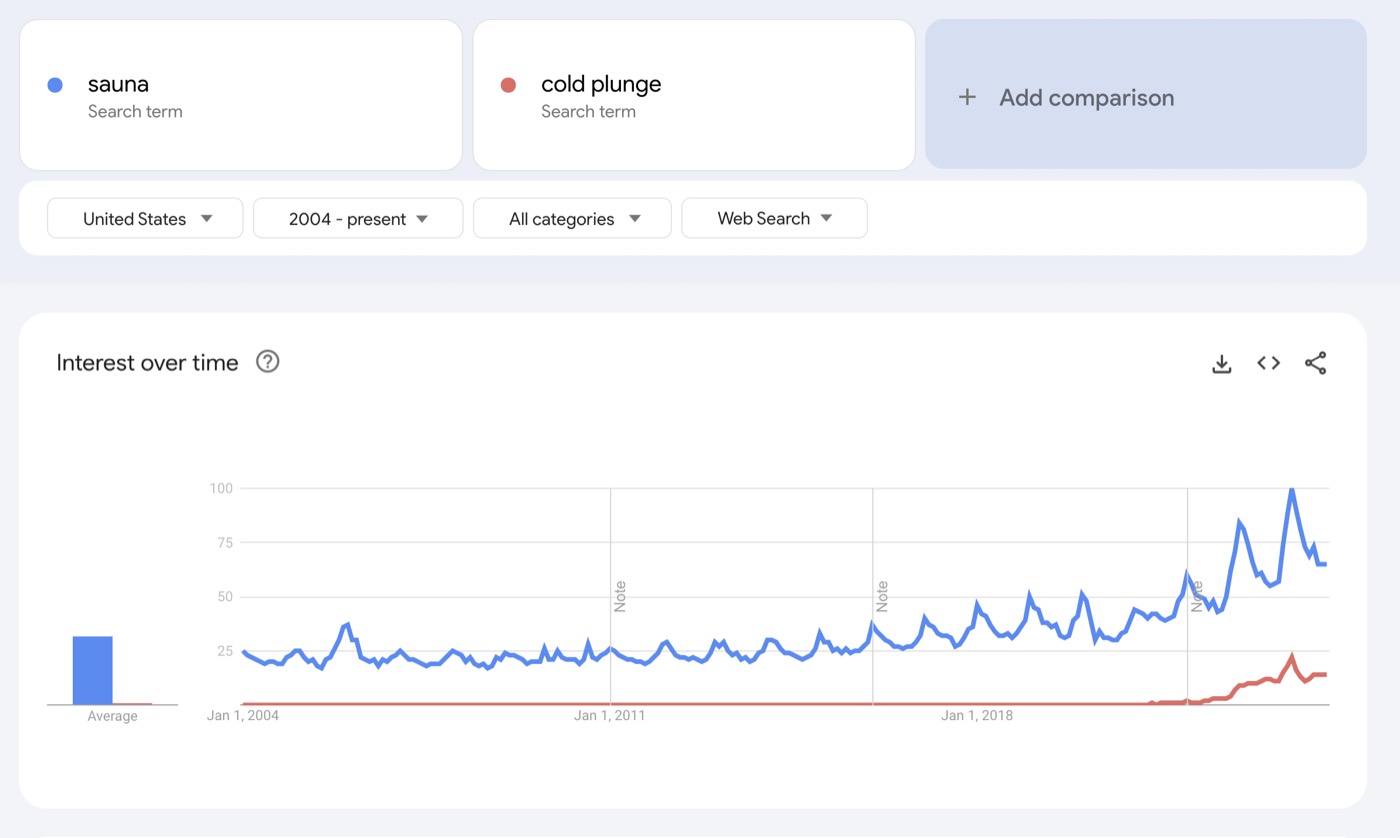

Demand signal

Post-COVID interest in sauna & cold plunge keeps climbing.

Bloomberg feature on the bathhouse/sauna/cold-plunge boom (Jan 2026); Fitt Insider (2025); Technavio US sauna market; Grand View Research cold-plunge market. The modern social bathhouse is a named 2026 wellness trend.

The Phoenix opening

The founder's thesis — that Phoenix wellness is all function, no form — holds up. In a metro of 5.2M (10th-largest, one of the fastest-growing in the US), there is no Japanese or communal, design-led bathhouse. The field is function-first chains and resort spas you can only enter by booking a treatment.

| Venue | Type | Entry | Positioning |

|---|---|---|---|

| Hot Water (proposed) | Japanese communal bathhouse + tea + retreat | — | Design-forward, social, cultural — the open lane |

| SweatHouz | Infrared sauna + cold plunge | ~$40 | Private clinical suites, membership chain |

| Optimyze (N. Phoenix) | Cold plunge / sauna / red light | $35–69 | Recovery studio, function-first |

| The Phoenician / Joya Spa | Resort spa (Joya = hammam) | treatment req. | Upscale, but you must book a treatment to enter; not East Asian |

Phoenix market scan, 2026 (operator sites). Nearest onsen-style venue is Castle Hot Springs, ~1 hr away. Climate angle: desert heat makes cold plunge & cool water viscerally appealing. Caveat: contrast therapy is competitive — the edge is experience and form, not the sauna/plunge function the chains already commoditize.